Since November last year when accelerated vaccine approvals gave the world a clear path out of the COVID pandemic, investors have constantly been searching for “re-opening” beneficiaries; stocks whose operations took a hit during enforced lockdowns and travel restrictions but should ride the tailwinds of pent-up demand as normality resumes.

The market was quick to find the obvious beneficiaries and re-price them accordingly such as travel, hospitality and tourism stocks. However, other not so obvious beneficiaries continue to seemingly offer value to investors willing to dig deeper and understand their business models and industry dynamics post-Covid. I believe one such example is Kip McGrath Education Centres.

Kip McGrath Education Centres (ASX: KME)

Kip McGrath is a leading provider of tutoring services to K-12 students, primarily in Maths and English. The business was founded by Kip McGrath in 1976 and has expanded from one tutoring centre in Maitland, NSW to 537 centres in 11 countries (primarily Australia and the UK) largely through a franchise business model. It is currently managed by Kip’s son Storm, with the father and son duo still owning around 30% of the business between them.

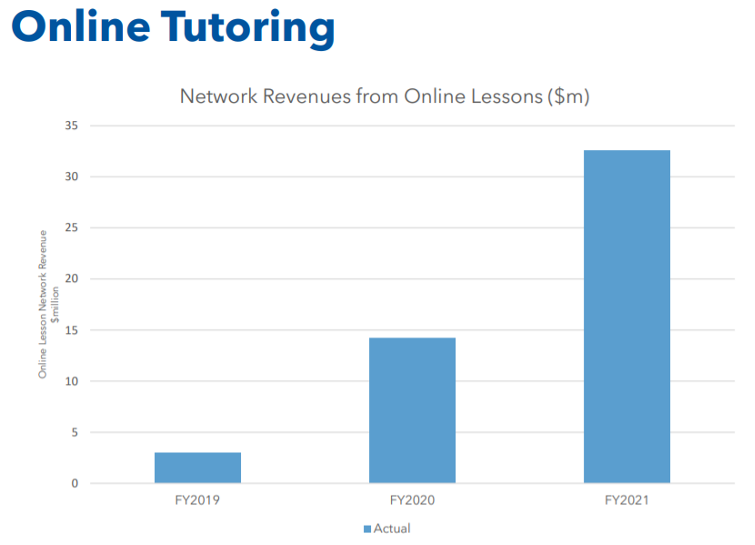

COVID brought significant disruption to Kip McGrath’s business, with lockdowns and travel restrictions meaning face to face tutoring became impossible. Kip McGrath had been developing their Kip Online system for some years prior to COVID, but penetration was minimal as tutors and parents/students were generally wary of the learning outcomes compared to face to face lessons. Pre-COVID, just over 1% of lessons were hosted online, but as tutors and students were forced online during COVID in FY21 that number was 40% of lessons.

Even as restrictions ease management expect 20-40% online penetration moving forward as more parents/students accept the quality of the Kip Online offering. The chart below highlights the rapid adoption of online lessons within Kip McGrath’s business:

The successful pivot to online learning means Kip McGrath’s revenues were not impacted dramatically through COVID (total FY21 network revenues fell 1%), and perhaps explains why it is not viewed as a COVID beneficiary by the market.

However, I expect Kip McGrath can now dramatically expand its addressable market, as previously the business was geographically constrained to areas where it had physical tutoring centres. However, now with an accepted online offering, Kip McGrath can market its services to parents and students outside of their centre catchment areas.

Beyond Kip McGrath expanding its own addressable market, I also expect the size of the private tutoring industry to grow strongly as parents look to ensure their children have not fallen behind after two years of disrupted learning. State Governments are already acknowledging this issue and Kip McGrath was one of a handful of tutoring companies selected in the NSW Government’s $337m Covid tutoring support package. Victoria has a similar package for $250m and other states are expected to follow.

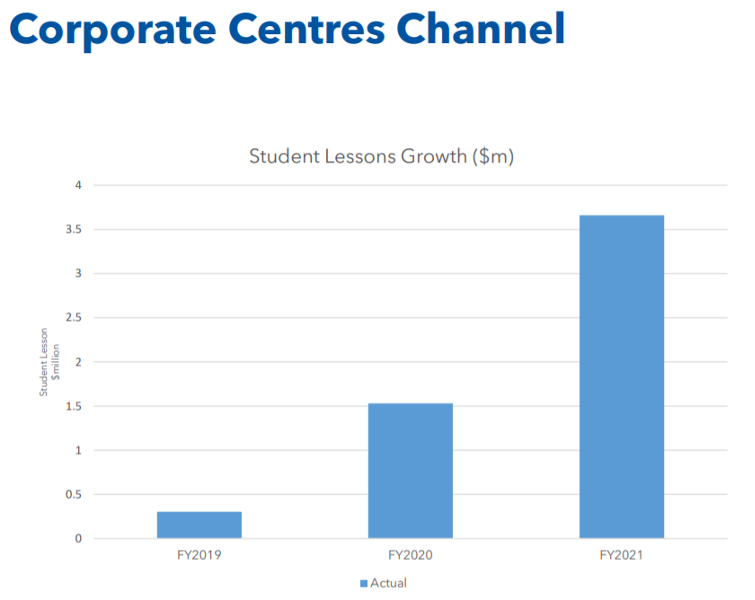

Servicing students outside of a centre catchment is also much easier as Kip McGrath has been developing a corporate channel to employ tutors and engage students directly (rather than through a franchisee). Driving this has been strategically identifying that certain centres in highly populated areas are more profitable if they are run by the corporate office rather than a franchisee. Kip McGrath has been purchasing these centres and using the tutors to service online students outside of catchment areas.

Management is expecting corporate revenue to more than double year on year in FY22 to over $7 million, and like online penetration, management is hoping to achieve a corporate/franchisee balance of 20-40% over time (currently 4%):

With online lessons and corporate centres driving significant revenue growth in the coming years, Kip McGrath will be able to sharply expand profit margins. Without the fixed overheads of physical centres, online lessons offer higher margins as Kip McGrath charges the same amount per lesson regardless of whether it is online or face to face. Also, by targeting only the most profitable centres, growth in corporate centre revenue will grow margins at the group level despite Kip McGrath taking on direct costs of running a centre.

Further, management invested heavily in the business in FY21 to accommodate the rapid pull forward of its long-term business plan to be a hybrid online/face to face learning business, ramping up spending in the Kip Online platform and fleshing out the executive team. With that platform now in place, revenues can scale substantially over the cost base.

Pre-COVID, Kip McGrath was growing its revenues around 25% and recorded $16.2 million in FY19. Management was in the process of investing in the Kip Online system which hit profit margins a little, but net profits still grew around 17% to $2.7 million. At the current market value of around $51 million, Kip McGrath trades on roughly 19 times its pre-COVID earnings. This seems fair value, but as I’ve outlined above, COVID has accelerated the growth drivers for the business.

I believe this will drive a step-change in profits over the next couple of years. I forecast the business achieving roughly $5 million in net profits in the next couple of years, which should drive great returns for shareholders from these levels.

Luke Winchester, Inception Fund Portfolio Manager

This post was also featured on Livewire (https://www.livewiremarkets.com/wires/the-re-opening-play-hiding-in-plain-sight)